Santander 2023

In this backtest, we are looking at Santander, the Spanish multinational financial services company based in Madrid. The data was pulled on 29 October 2024. When environmental issues are material for companies that perhaps wouldn't expect it.

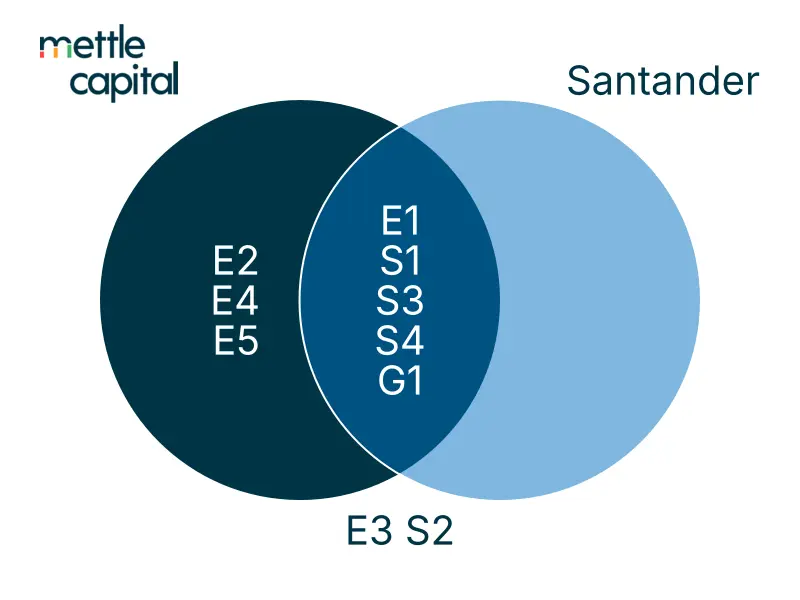

Alignment of Topic Materiality

Comparing the two assessments, there is significant agreement in which topics are material and which are non material. Within ESRS reporting, E2 Pollution, E4 Biodiversity and E5 Resource Use might not feel particularly material to a bank. But our materiality assessment suggests there are significant conversations about Santander in exactly these areas, which haven't been included in their (voluntarily reported) annual report. And while we agree that G1 Business conduct is important to include, there is a significant recent increase in data around the sub-topic corruption and bribery.

Topic Materiality over time

2023

2024

S4 Consumers and end user, E4 Biodiversity have become more material since Dec 2023. G1 Business conduct has become more material while E5 Circular Economy has become less material. There is evolution within the subtopics, which will impact on IRO reporting.

Which sub-topics are showing shifts in materiality

G1.6 Corruption and Bribery has increased in materiality significantly. A fuller comparison with peers/subsector would show whether Santander is an outlier or not on the most material subtopics.

Materiality of Non-ESRS subtopics

Developed using SASB taxonomy and Mettle's own unique Trust, Reputation, Thematic models. The taxonomies intentionally have some overlap with each other and with the ESRS taxonomy. Key to this analysis is identifying new topics not specified in ESRS, but meeting the requirement to determine anything else that is material. We would also suggest including Innovating, Privacy as being material to full CSRD reporting.