OSMA Four Steps

Aligned with EFRAG guidance

Four Step Process

The guidance sets out the four steps of a materiality assessment. [1] The example below is the open source materiality assessment for Orsted, the Danish energy company, for the period 1 January 2023 - 31 December 2023.

Step A - Understand the context

Open source materiality assessment (OSMA) combines three datasets to provide a comprehensive understanding of the context:

Internal

Users upload their company's latest annual report as a pdf which is instantly machine read against the ESRS (and other) taxonomies.

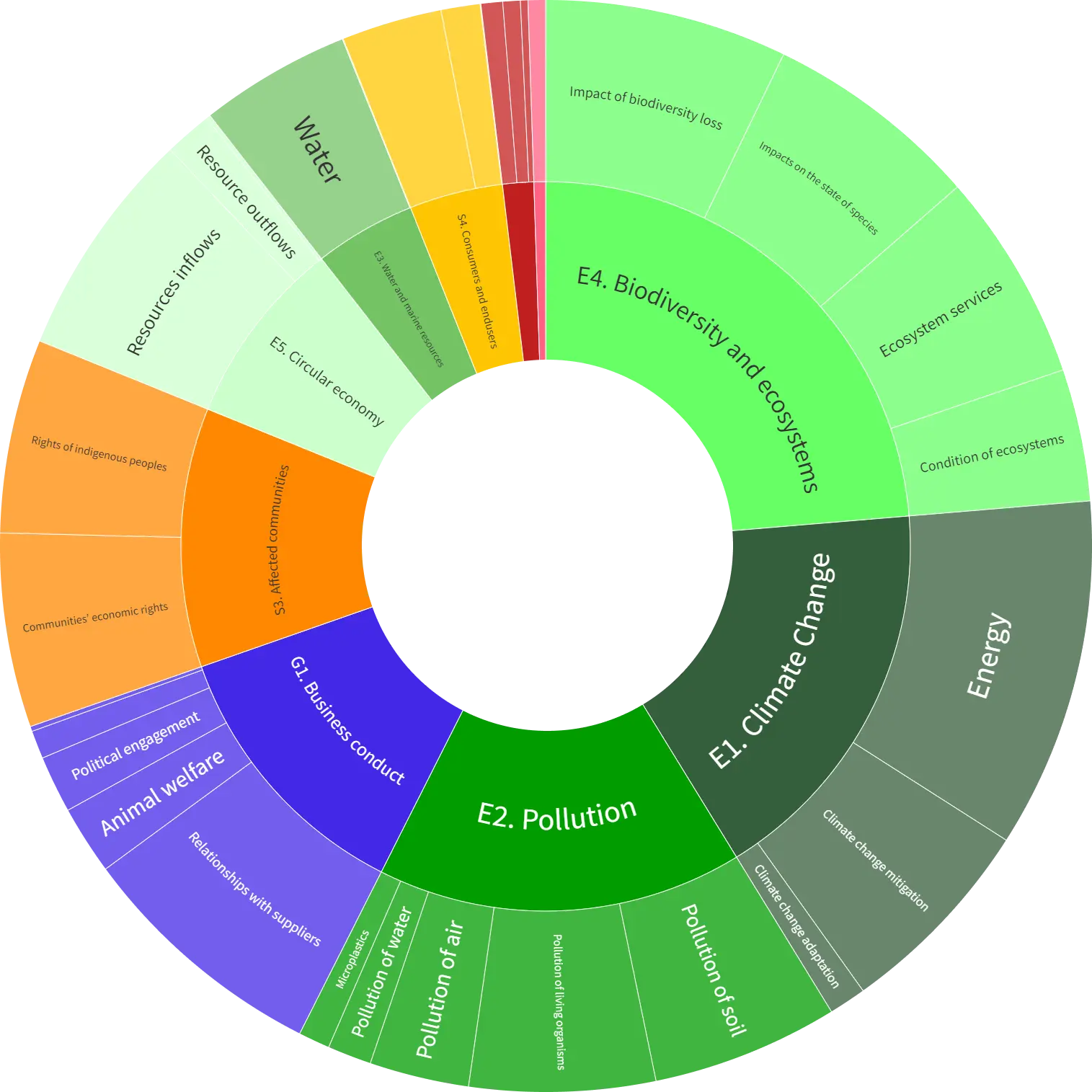

In this dataset, E4. Biodiversity and ecosystems is the most material topic, E1. Climate Change is the second, and E2. Pollution the third most material topics.

External

Mettle sources traditional, trade and social media in local language relevant to the company. Traditional media includes major media outlets like BBC, Financial Times, The Economist. Trade includes industry-specific publications like Fierce Pharma, Retail Week as well as regulatory news. Social media includes forums, blogs by subject matter experts as well as relevant Twitter and Reddit. Languages currently include: English, Spanish, German, Italian, French, Dutch, Danish, Norwegian, Swedish, Finnish and Polish.

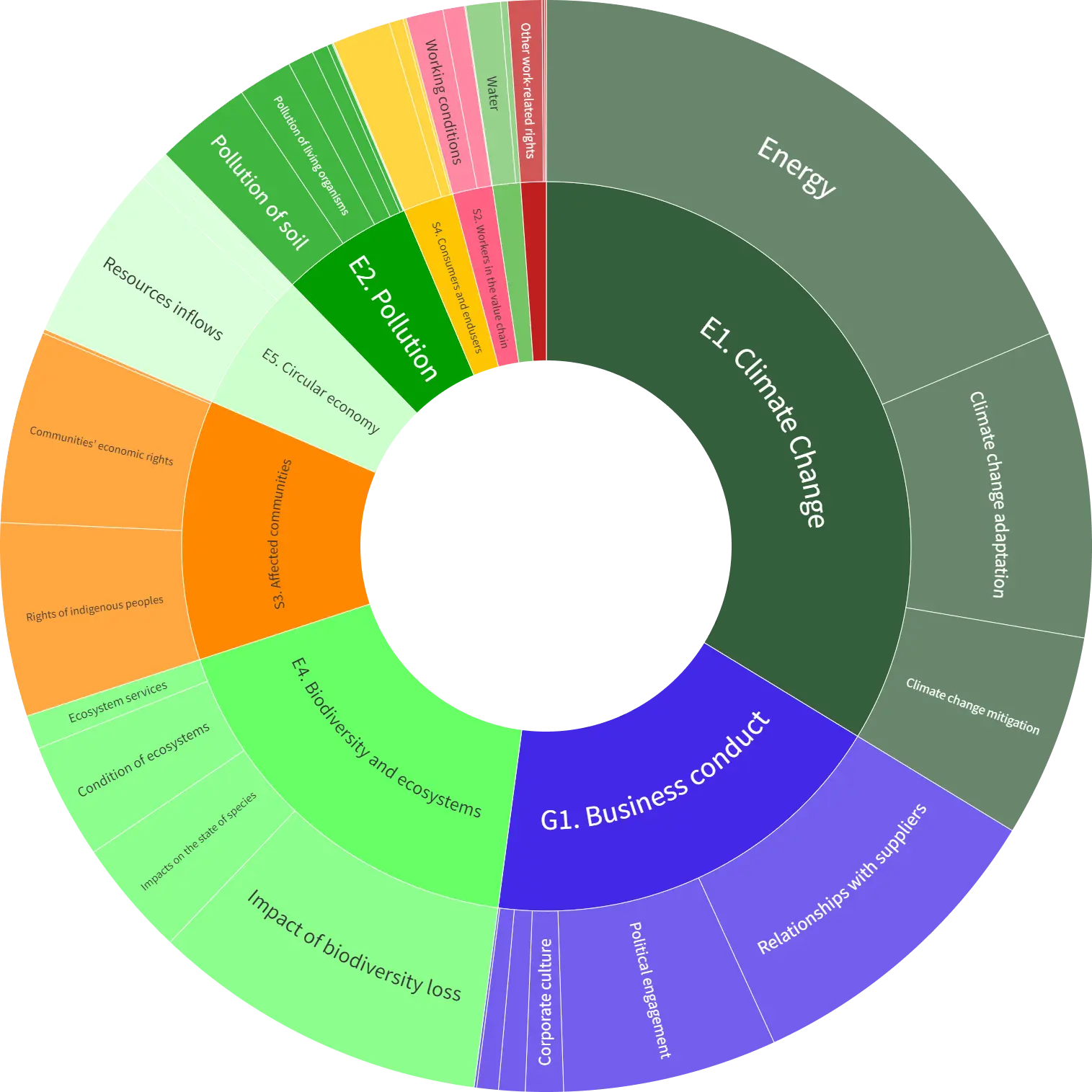

In this dataset, E1. Climate Change is the most material topic, G1. Business conduct is the second, and E4. Biodiversity and ecosystems the third most material topics.

Industry

Mettle collects data on the largest 5,000 companies in the EU and US. These are tagged against 77 industries. The third data set is all the traditional, social, and trade media in local language on all the companies in the relevant industry.

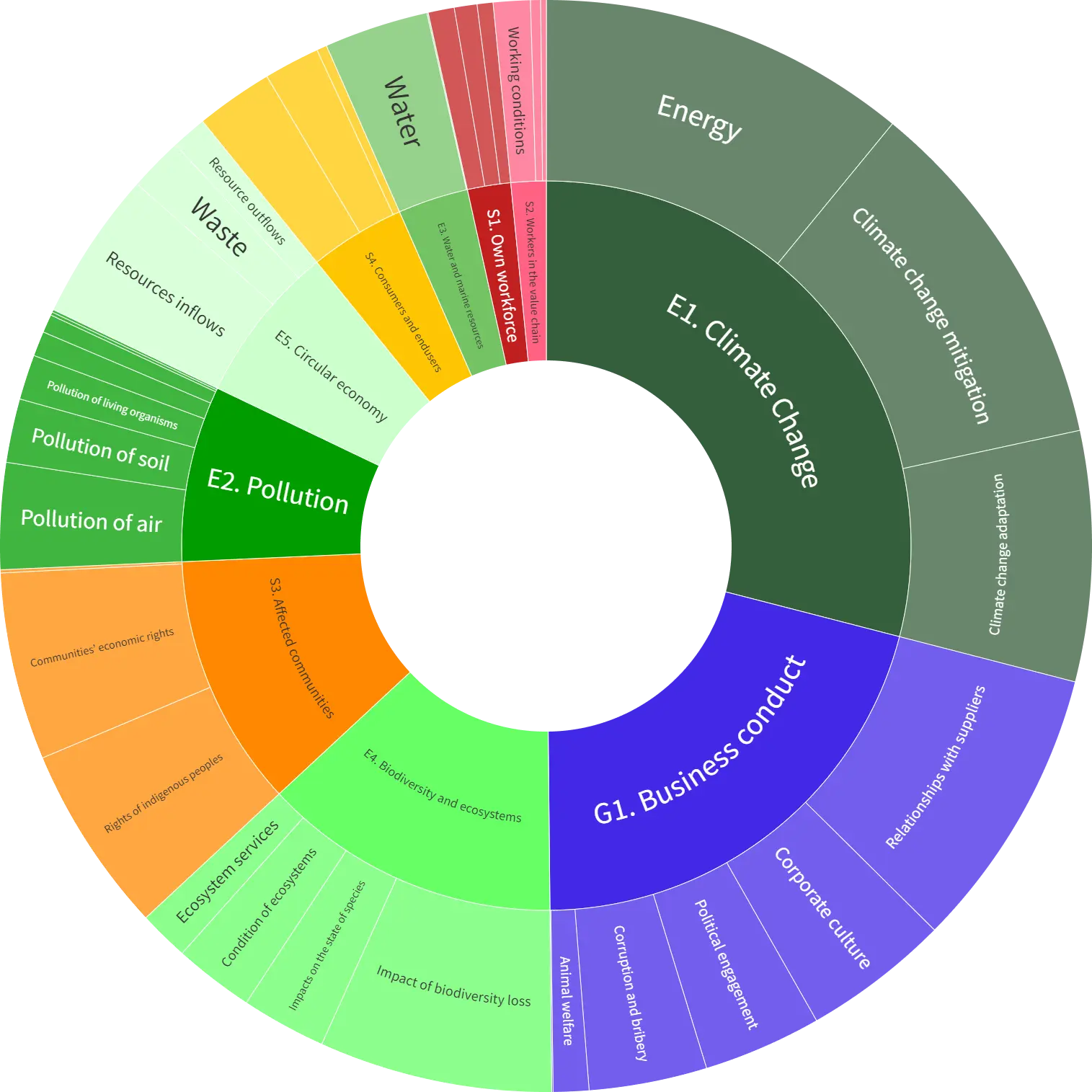

In this dataset, E1. Climate Change is the most material topic, G1. Business conduct is the second, and E4. Biodiversity and ecosystems the third most material topics.

Step B - Identify which topics are relevant for your company

The three datasets are combined at the identify stage. The datasets are equally weighted. Deploying three datasets enables the preparer to more fully identify the material risks and opportunities at subtopic level. If the company has relatively little External data, the Internal and Industry datasets combined are sufficient for a robust analysis.

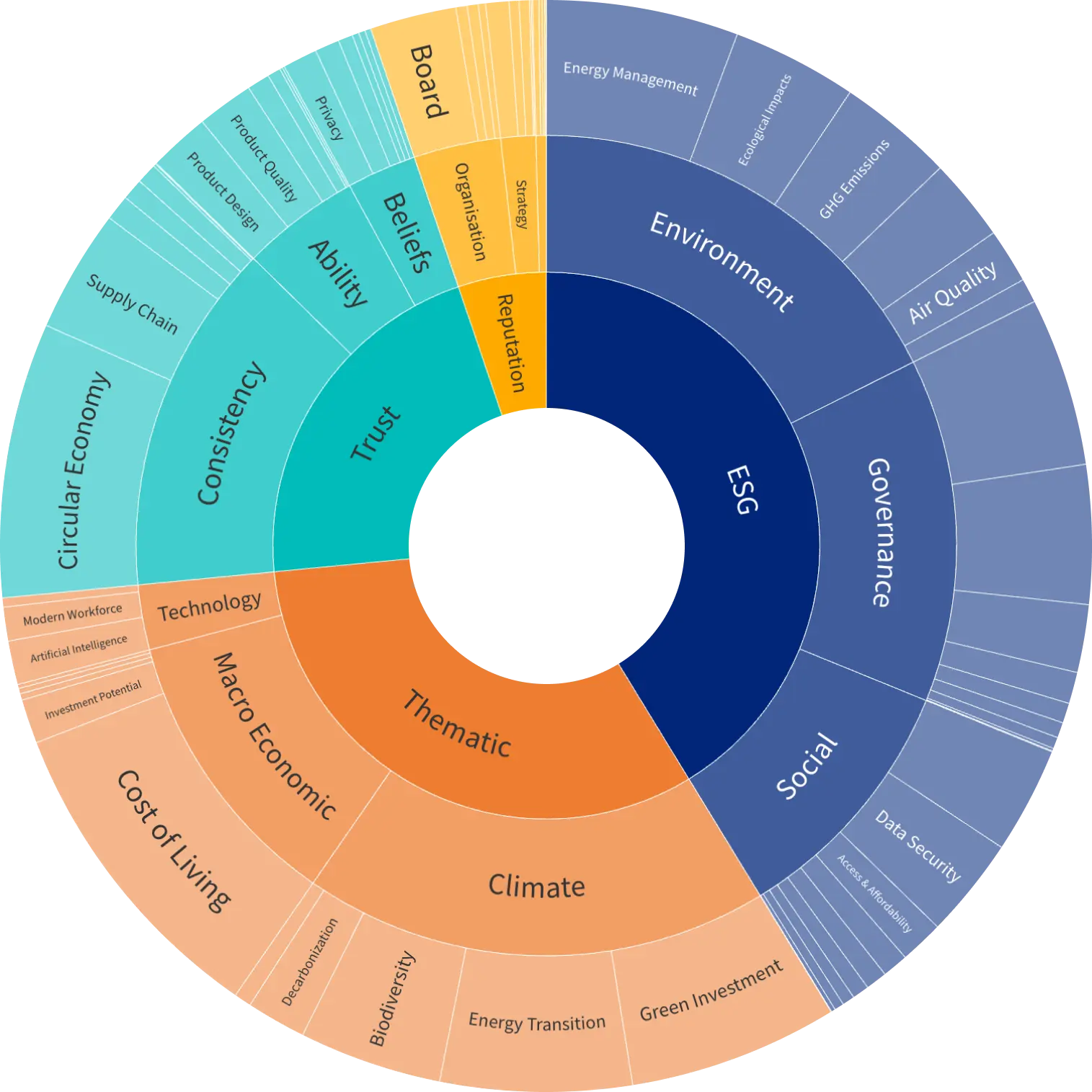

The guidance is clear [2] that the preparer needs to look beyond just the ESRS taxonomy for entity-specific issues that may be material. Mettle also runs four other taxonomies - ESG(ISSB), Reputation, Trust, Thematic - in order to meet this requirement.

ESRS Taxonomy

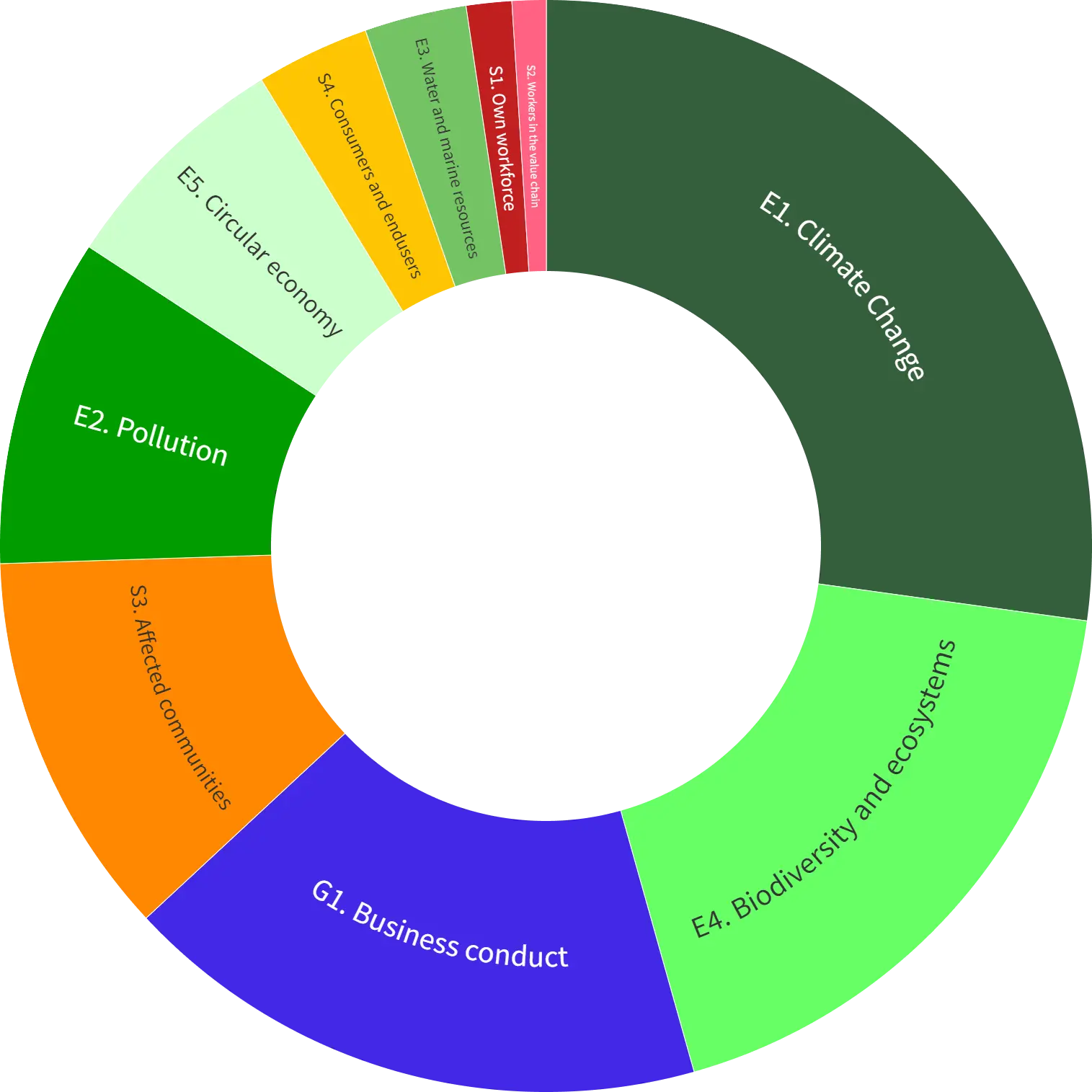

The Internal, External and Industry materialities are combined. This shows the relative materiality of all the topics and subtopics in context, ready for assessment in the next stage of the process.

In this combined dataset, we see that E1. Climate Change is the most material topic overall, E4. Biodiversity and ecosystems the second, and the G1. Business Conduct the third most material topics.

Broad Taxonomy

Deploying a broad taxonomy of 12 topics and 79 subtopics, the Internal, External and Industry materialities are combined. Any material topics/subtopics identified here are added to the assessment in the next stage of the process.

In this broader dataset, we see material subtopics that need to be in assessed in the next step, for example Cost of Living. Some subtopics are already included in the ESRS taxonomy, for example Circular Economy.

Step C - Assess the risks and opportunities of those topics

The dashboard allows preparers to drill down into each topic and subtopic to inform their assessment whether to include in the final report. Expert knowledge of the individual company is required here with Mettle dashboard providing data and evidence to help judge severity and likelihood.

The guidance requires the preparer to set "appropriate quantitative and/or qualitative thresholds for reporting purposes. Severity is based on the scale, scope and irremediable character of negative impacts and the scale and scope of positive impacts." [3] The data is presented in the dashboard to enable the preparer to set thresholds.

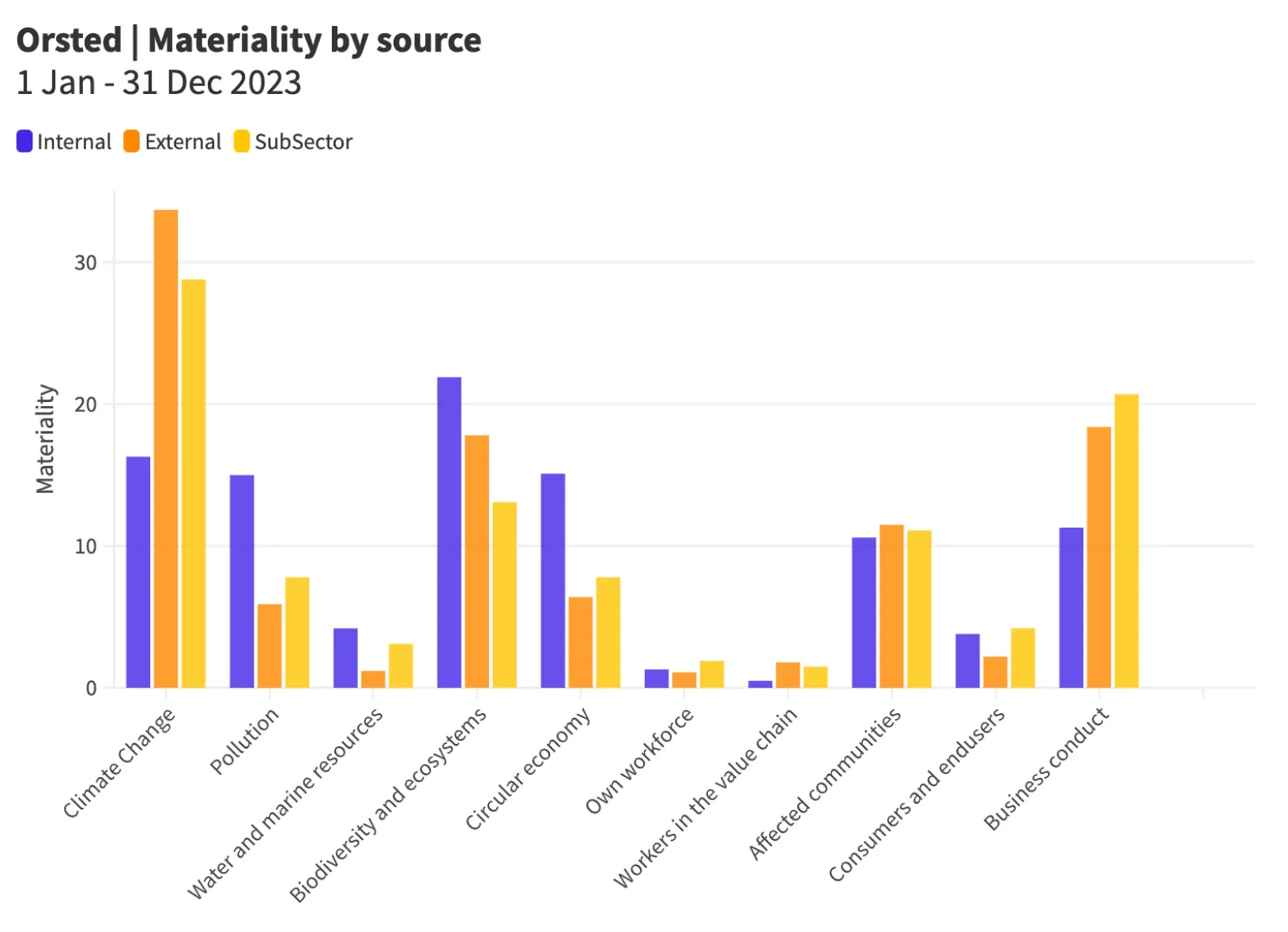

Materiality by source

This chart compares the Internal, External and Industry materiality weightings in order to assess the appropriate threshold for inclusion in the next stage.

In this combined dataset, we see that E1. Climate Change is the most material topic in External and Industry so should be included even though it is less material for Internal. This assessment can also be conducted at subtopic level for greater granularity.

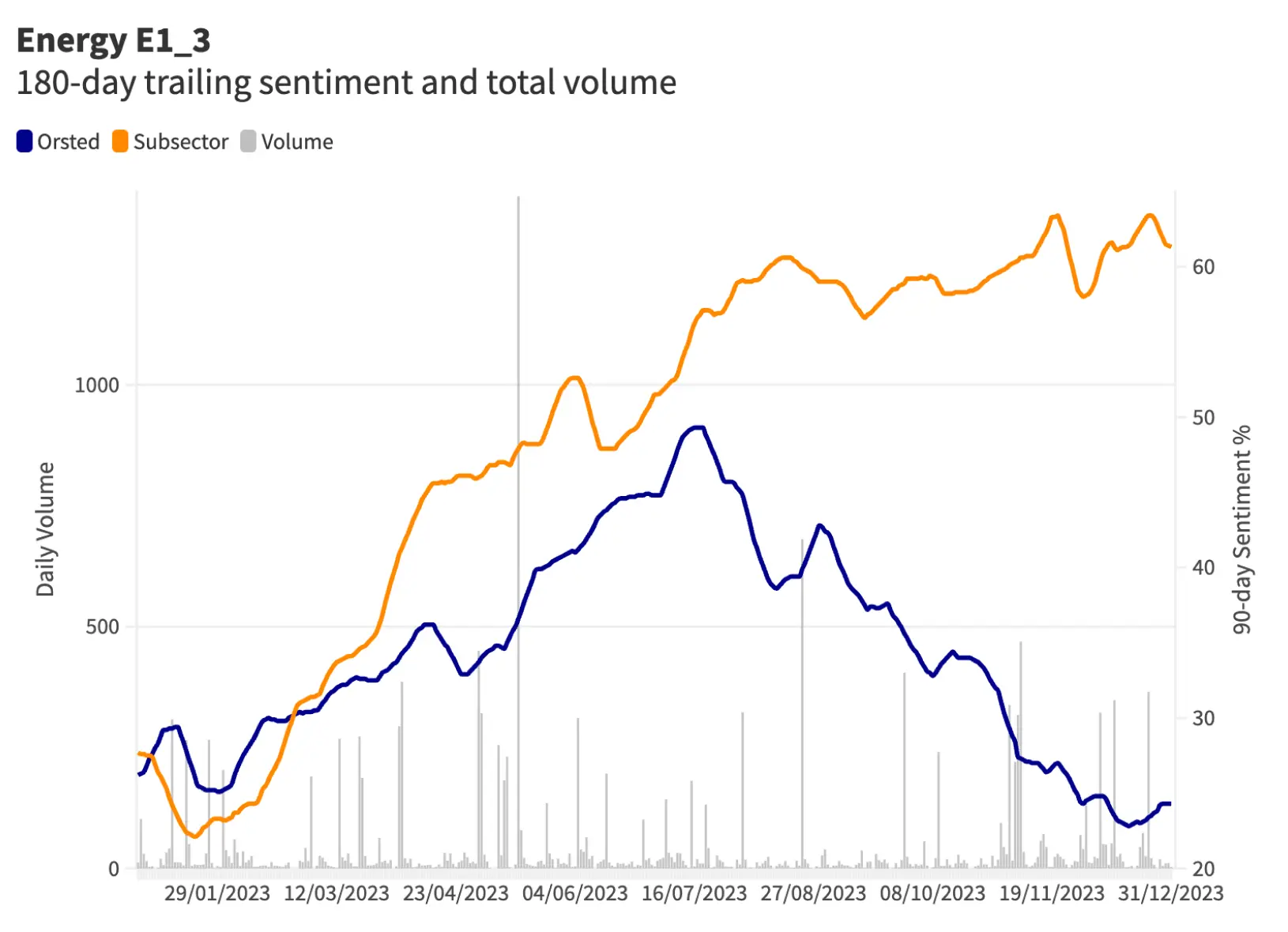

Drill down on Subtopic

Within the E1. Climate Change topic, Energy is the most material subtopic. "Energy" subtopic is defined in the taxonomy as covering energy-related matters, to the extent that they are relevant to climate change.

Drilling down on that subtopic, this chart shows stakeholders' sentiment of the company compared to industry. In this dataset, sentiment diverged half way through the period, indicating scale and scope of negative impacts.

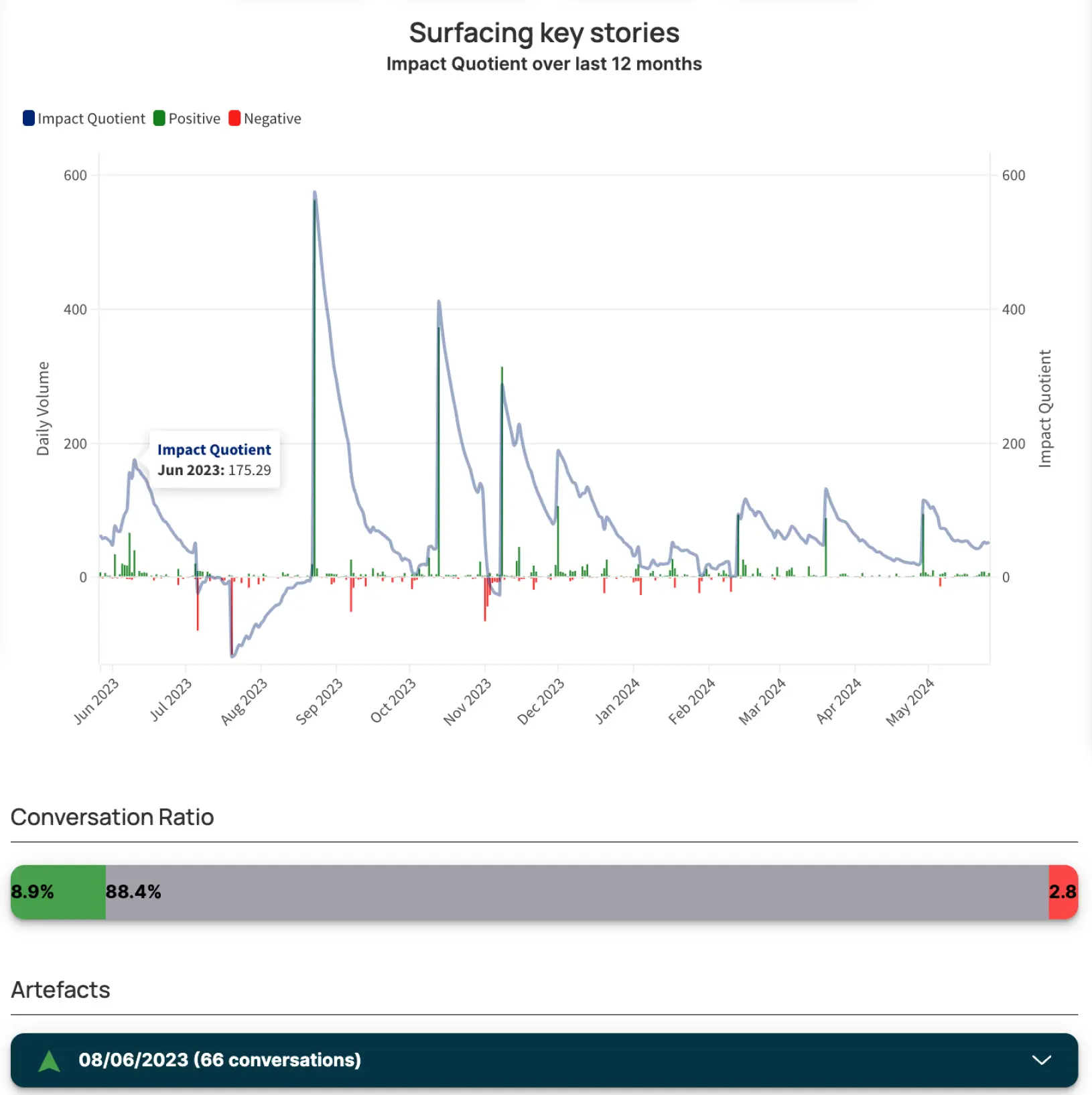

Isolate material issues

Following on from the previous chart, the dataset can be interrogated to understand the positive and negative stakeholder sentiment associated with the subtopic.

This data can inform a judgement about the irremediable character of negative impacts as well as the scale and scope of the positive impacts.

Step D - Report your results

The dashboard displays relevant ESRS data points for reporting on. The preparer includes all the relevant data points for each Disclosure Requirement judged material. The final list of IROs to be reported can be exported into the company"s current reporting software (e.g. Salesforce, Workiva) as required.

The topline materiality assessment is included in the annual report together with the final list of IROs and their disclosure requirements.

In this example, the material topics are E1. Climate Change, E4. Biodiversity and ecosystems, G1. Business Conduct, S3. Affect Communities, E2. Pollution, E5. Circular Economy. The other topics are not material and do not need to be reported.

Within each of the topics, the most material subtopics are assessed in the previous step. In this example, the "Energy" subtopic would be reported on as a material IRO although it may be consolidated in the final report.

The guidance highlights three additional disclosures that also need to be included. Mettle Capital provides standard wording to meet the requirements for ESRS 2 IRO-1 "Disclose the Process" and ESRS 2 SBM-2 "Stakeholder Engagement". The data in the dashboard can be used to complete ESRS 2 SBM-3 "Material IROs and their interaction with strategy and business model".